Offshore guarantees by Vietnamese Companies

Under the amended Ordinance on Foreign Exchange, a Vietnamese entity (Vietnamese Guarantor) can only guarantee for obligations of an offshore entity if it obtains an approval by the Prime Minister for doing so. Obtaining a Prime Minister’s approval makes it considerably difficult for a company in Vietnam to issue a guarantee for obligations of an offshore company (e.g. the parent company of a Vietnamese subsidiary). Circular 37/2013 of the State Bank of Vietnam (SBV) which takes effect from 14 February 2014 provides further guidance on an offshore guarantee by a Vietnamese Guarantor. In particular,

- Circular 37/2013 provides that the obligations to be guaranteed by a Vietnamese Guarantor need to be “financial obligations” (nghĩa vụ tài chính). There is no definition of financial obligations. It is not clear if this means that offshore guarantees for non-financial obligations can be issued without obtaining Prime Minister’s approval;

- Circular 37/2013 requires the Vietnamese Guarantor to open a special account to pay for the guaranteed obligations and to receive reimbursement payment by the guaranteed entity; and

- Circular 37/2013 requires the Vietnamese Guarantor to register the repayment obligations by the offshore guaranteed entity with the SBV after the Vietnamese Guarantor’s paying the guaranteed amount to the beneficiary.

In March 2026, Vietnam’s Ministry of Finance (MOF) released a draft decree (Draft Decree) implementing the Law on Personal Income Tax 2025 (PIT Law 2025) for public consultation. One proposal drew strong feedback from businesses and investors: a change to how individuals are taxed on the transfer of shares in non-public/unlisted joint-stock companies (JSCs). Following the consultation, the MOF now appears poised to step back from that change – welcome news for investors and companies engaged in M&A and private share transactions.

On 5 June 2026, the Government issued Decree 200 on private placement and trading of corporate bonds on domestic market and offering of corporate bonds on international market (Decree 200/2026). Decree 200/2026 will replace Decree 153/2020 on the same subject. In the past, Decree 153/2020 has been amended by Decree 65/2022 and Decree 8/2023. Decree 200/2026 introduces more conditions for private bond issuance.

5x debt/equity ratio

1.1. Decree 200/2026 reflects the 5x debt/equity requirement established under the 2025 amendment to the Enterprise Law. In particular, the debt of a bond issuer (including the value of the bonds to be issued) must not exceed 5 times of the equity of such issuer as recorded in the audited financial statements of the year preceding the issuance.

On 15 May 2026, the Ministry of Finance issued Circular 55/2026/TT-BTC (Circular 55/2026), introducing a new set of forms for investment activities in Vietnam. Two specific changes in the new form of application for M&A Approval are notable for investors engaged in M&A transactions.

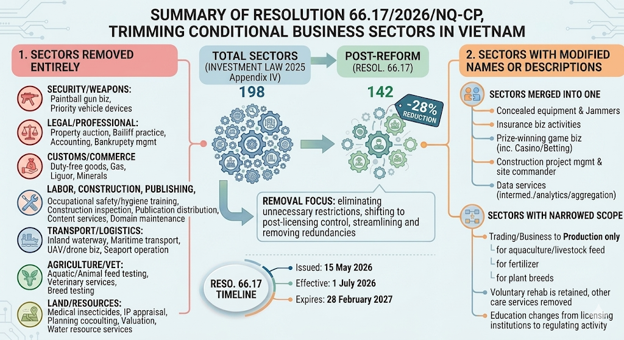

On 15 May 2026, the Government issued Resolution No. 66.17/2026/NQ-CP (the Resolution 66.17 or the new), slimming down the list of conditional business sectors currently set out in Appendix IV of Investment Law 2025 (the old).

Resolution 66.17 will take effect on 1 July 2026 and is set to expire on 28 February 2027, by which time the Government expects the National Assembly to formalise these adjustments through an amendment to Appendix IV. Although there would be a question about the effectiveness of the Resolution 66.17 over the Appendix 4 of Investment Law 2025 and how the investment authority will apply in practice, the investor may, in the meantime, treat the Resolution 66.17 as the working text for the next 9–10 months while following up on the law amendments.

Under Article 41 of the Law on Real Estate Business 2023 (Real Estate Business Law), a real estate project (Project) eligible for transfer may follow one of two sets of legal procedures, depending on how it was approved. While the difference may appear procedural at first glance, it has significant implications for when the transfer transaction is legally completed, and for what the parties can (or cannot) do if the transaction ultimately falls through. This post discusses the two procedures and the practical implications arising from the distinction between them.

Vietnam has temporarily raised several general economic concentration notification thresholds under Resolution No. 66.18 of the Government dated 18 May 2026 (Resolution 66/2026), a practical change for M&A transactions as fewer deals should be caught solely by Vietnamese assets, Vietnamese turnover or transaction value.

On 3 September 2025, the Ministry of Finance (MOF) released the Official Letter no. 13629 addressing questions related to difficulties and obstacles arising from legal regulations in the finance and investment sector. This correspondence has several notable issues that are summarized below. While some of the MOF’s guidance offers welcome flexibility and operational reassurance, others fall short of providing clear or comprehensive clarification, leaving important gaps unresolved and inconsistencies with other legislation unaddressed.

Delegation by the General Meeting of Shareholders endorsed in principle (Query no. 29)

Query/Issue raised:

Current regulations regarding delegation/authorisation (both could be translated to/from "uỷ quyền" in Vietnamese) by the General Meeting of Shareholders (GMS) to the Board are unclear and conflicting. […]

A recurring issue in Vietnam corporate governance is whether a former member of the Board of Directors can be appointed as an “independent” Board member in the subsequent term, provided that all other statutory criteria are satisfied. This typically arises where companies want to retain a former board member while still complying with independence requirements under Article 155.2 of the Enterprises Law 2020 as amended in 2025 (Enterprises Law 2020).

Under Article 155.2(dd) of Enterprises Law 2020, an independent Board member must “not hold the position of member of the Board of the company within the last 05 years or longer unless he/she was designated in 02 consecutive terms.”

Vietnamese law currently lacks a formal definition of “latent defect” (khiếm khuyết ẩn) and a clear mechanism for allocating liability once such defects arise. This regulatory vacuum often leads to prolonged disputes between the Employer and the Contractor, particularly when the construction contracts do not include explicit risk allocation.

For the purpose of our discussion below, a “latent defect” is defined as a fault or flaw in construction works/item that is not discoverable through a reasonably thorough inspection at the time of handover.

The Government officially issued Decree 102/2026/NĐ-CP (Decree 102/2026), which introduces critical amendments and supplements to Decree 75/2019/NĐ-CP (Decree 75/2019) regarding administrative penalties for violations in the competition sector. Effective from 20 May 2026, Decree 102/2026 provides clearer enforcement guidelines and adjusts penalty frameworks, particularly for economic concentrations.

Below is a summary of the key changes introduced by Decree 102 that will directly affect M&A transactions subject to merger control (economic concentration notification) requirements in Vietnam.